Blog

When it comes to building tax-free retirement savings, two of the most powerful tools available are the Roth IRA and the Roth 401(k). Both are funded with after-tax dollars, meaning you don't get a tax break upfront — but your money grows tax-free, and qualified withdrawals in retirement are tax-free as well.

While they share that core benefit, they differ in important ways that affect who can use them, how much you can contribute, and how they fit into your overall retirement strategy.

Roth IRA: Flexibility with Limits

A Roth IRA is an individual account you open on your own through a brokerage, bank, or other financial institution. It offers significant flexibility in how you invest your money, with access to a wide range of stocks, ETFs, mutual funds, and bonds.

Key advantages:

- No required minimum distributions (RMDs) during your lifetime, making it a powerful tool for long-term wealth building and estate planning

- Wide investment selection — you choose the provider and the investments

- Contributions can be withdrawn anytime tax- and penalty-free (earnings have stricter rules)

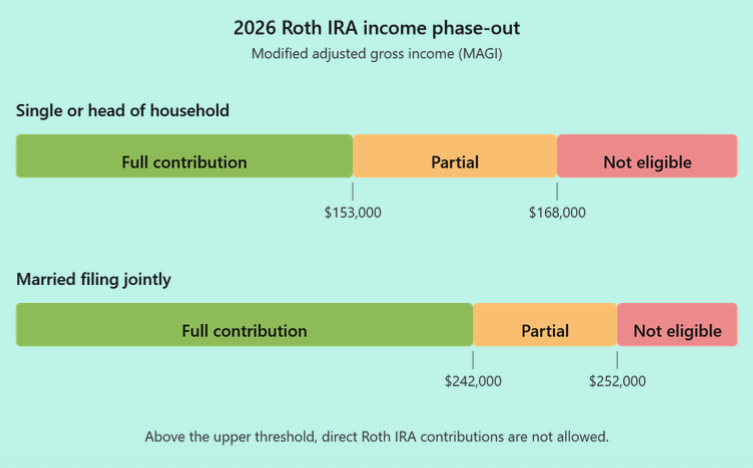

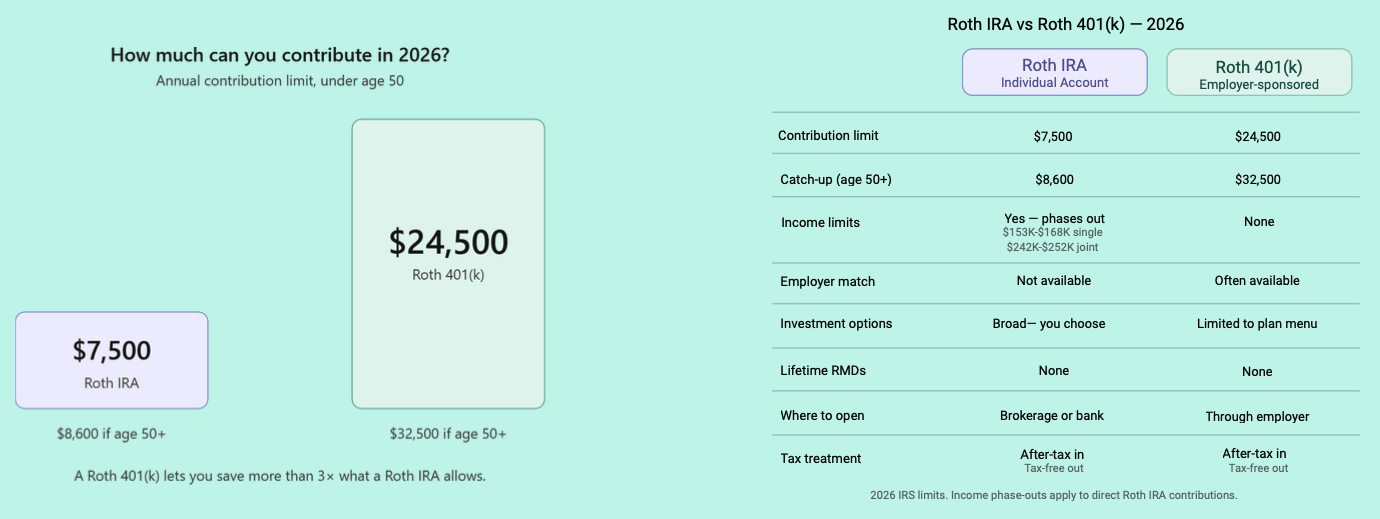

The catch — income restrictions: For 2026, your ability to contribute directly to a Roth IRA phases out at certain income levels. Single filers begin to phase out at $153,000 of modified adjusted gross income (MAGI) and are completely phased out at $168,000. For married couples filing jointly, the phase-out range is $242,000 to $252,000.

Roth IRAs have relatively low contribution limits — $7,500 in 2026, or $8,600 if you're 50 or older.

Roth 401(k): Higher Limits, No Income Cap

A Roth 401(k) is offered through your employer and works on the same basic principle: after-tax contributions, tax-free growth, and tax-free qualified withdrawals.

Key advantages:

- No income limits — you can contribute regardless of how much you earn

- Much higher contribution limits — $24,500 in 2026, or $32,500 if you're 50 or older (with an even higher "super catch-up" of $35,750 available for ages 60–63 under SECURE 2.0)

- Employer matching may be available, adding free money to your retirement

A few things to note: SECURE 2.0 now allows employers to offer Roth matching; however, not all Roth 401(k) plans have adopted this feature. Traditionallly employer matching contributions were made on a a pre-tax basis. Ask your plan administor if the plan allows for Roth matching by the employer. Investment options are typically limited to whatever menu of funds your employer's plan offers, which may be more restrictive than what you'd find in a Roth IRA. And while RMDs used to apply to Roth 401(k)s, SECURE 2.0 eliminated lifetime RMDs starting in 2024, putting them on equal footing with Roth IRAs in that respect.

The Key Takeaway: Access Is Everything

The most important distinction between these two accounts is access. A Roth IRA can be limited or eliminated entirely by your income, while a Roth 401(k) has no income cap. That means if you earn too much to contribute directly to a Roth IRA, you can still contribute to a Roth 401(k) if your employer offers one — and you can contribute substantially more. For many high earners, the Roth 401(k) becomes the simplest and most powerful way to keep building tax-free retirement savings once Roth IRA eligibility phases out.

And remember: you don't have to choose just one. If you're eligible, contributing to both can be a smart way to maximize your tax-free retirement wealth.